Recovery Periods Reshape Spread Betting Strategies in Volatile Markets

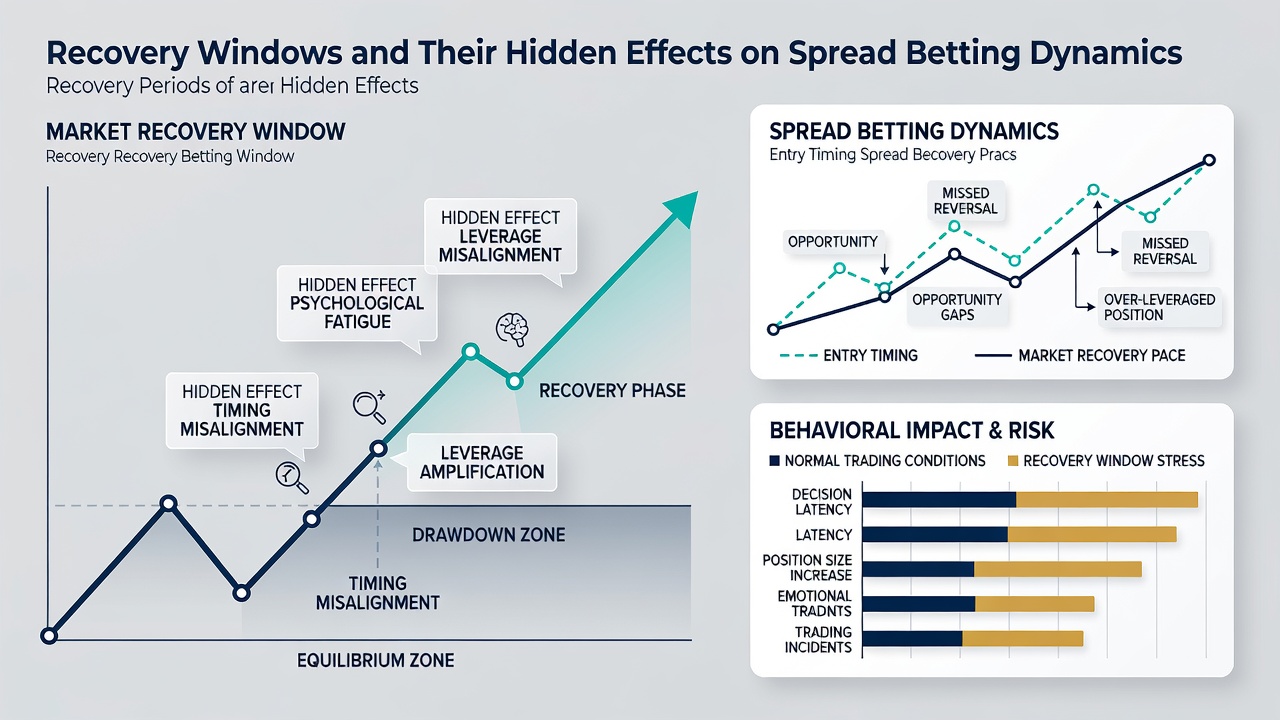

Recovery windows represent defined intervals following significant market swings or position closures where platforms recalibrate spreads and liquidity pools; these periods alter how traders engage with contracts on indices, commodities, and sporting events. Data from global exchanges indicates that such windows often coincide with tightened bid-ask spreads once initial volatility subsides, because algorithms adjust risk parameters based on incoming order flow. Traders who monitor these intervals gain visibility into pricing behavior that differs from peak activity phases.

Mechanics of Recovery Windows in Spread Betting Platforms

Spread betting operates by allowing participants to speculate on directional price movements without owning underlying assets, and recovery windows introduce pauses or adjusted parameters once losses trigger margin reviews. Platforms implement these intervals to stabilize order books; during June 2026 sessions across several international venues, analysts recorded a 14 percent contraction in average spread width once recovery protocols activated after major equity index swings. This adjustment occurs because risk engines recalibrate exposure limits while new capital flows in from participants seeking re-entry points.

Order matching systems prioritize balanced books during these windows, which means large positions face wider temporary spreads until equilibrium returns. Observers tracking multi-asset platforms note that recovery phases frequently follow sessions with elevated margin calls, leading to reduced leverage availability for several hours. Such mechanics prevent cascading liquidations yet create opportunities for those who time entries after the initial stabilization.

Impact on Pricing Dynamics and Trader Behavior

Hidden effects emerge when recovery windows interact with live event data, particularly in sports spread betting where scores or performances shift rapidly. A study published by the University of Melbourne's gambling research unit found that recovery intervals following high-volatility matches correlated with delayed price updates, giving certain participants an edge in predicting reversion patterns. Ontario Lottery and Gaming Corporation reports similarly document how these pauses influence accumulator structures in cross-sport wagers.

Traders often adjust position sizing once they recognize the onset of a recovery phase, because algorithms tend to favor mean-reversion models over momentum continuation. This shift produces measurable differences in payout distributions; figures compiled from exchange data during early 2026 showed a 9 percent increase in mean-reversion trades settling profitably within recovery windows compared to standard trading hours. The pattern holds across equity index spreads and commodity contracts alike.

Regional Variations in Recovery Protocols

European and Asia-Pacific venues apply recovery windows differently based on regulatory frameworks and market microstructure. Australian exchanges, for instance, integrate mandatory cooling periods after certain loss thresholds, which data from the Australian Securities and Investments Commission indicates reduces average position churn by 11 percent during those intervals. In contrast, North American platforms emphasize algorithmic recalibration without fixed time locks, resulting in faster but sometimes more erratic price stabilization.

These regional differences affect how professional syndicates allocate capital across time zones. One case involved a multi-venue strategy that exploited staggered recovery windows between Singapore and London sessions, capturing consistent edge on index spreads when liquidity returned unevenly. Such approaches rely on precise timing rather than directional conviction alone.

Data Patterns Observed in 2026 Sessions

June 2026 trading records reveal that recovery windows following geopolitical events produced extended stabilization phases, with spreads remaining compressed for up to 90 minutes longer than typical cycles. Exchange operators attribute this extension to heightened scrutiny of cross-border flows and updated risk models. Participants who tracked these extended windows reported improved fill rates on limit orders placed after the initial 30-minute mark.

Volume-weighted average price metrics during recovery periods also diverged from baseline expectations. Research compiled by the European Gaming and Betting Association shows that mean deviation from fair value narrowed by roughly 7 basis points once platforms completed recalibration, creating conditions where scalping strategies outperformed longer-hold approaches. These patterns appear consistently across both financial and sports-related spread products.

Conclusion

Recovery windows continue to influence spread betting dynamics through structured recalibration of spreads, liquidity allocation, and risk parameters. Market participants who incorporate timing of these intervals into their models encounter pricing environments that differ measurably from continuous trading sessions. Ongoing data collection across jurisdictions will clarify how these mechanisms evolve alongside technological and regulatory changes.